So, as the fund's share of equity rises, the could you be more of a wesley fee rises. This suggests you obtain some money back if you market your house earlier than anticipated. The quantity you come back depends upon when you market your house and just how much you got for your offered share. You might also have the choice to buy back the offered share later, if you desire. You can pick from a number of terms, such as three-year and five-year and can choose fixed or variable prices.

If the securities market collisions, he frets much less, he will certainly not take out from retired life funds, he will certainly make withdrawals from the line of credit that year or those years. If a reverse mortgage loan provider tells you, "You will not lose your house," they're not being straight with you. You absolutely can lose your residence if you have a reverse mortgage. If you're 62 or older, you can qualify for an HECM car loan as well as use it for any type of function. Some folks will use it to spend for bills, getaways, home renovations and even to pay off the remaining amount on their routine mortgage-- which is nuts!

Your loan provider may also ask you as well as the various other individuals to get independent legal suggestions. They might ask for evidence that you got this suggestions. In 15 years, if their residential or commercial property rises in worth 3% annually, it will certainly deserve $779,984.

- You can still leave the residence to your beneficiaries, however they will have to repay the car loan equilibrium.

- Most 62 year olds aren't mosting likely to be able to do the math to actually know which alternative appears in advance, right?

- Please talk to your Rothenberg Wide range Management expert for advice based upon your unique situations.

- An integral part of reviewing whether a reverse mortgage is best for you or not is figuring out why you really need the funds.

If you have actually faced difficulties coming up with the cash for these necessary costs, adding to your debt ought to not get on the table. Instead of making a settlement each month, you will pay nothing. The rate of interest price is included in the home loan balance, so in the second month, the balance grows. Considering that the lending equilibrium is now a little larger, the interest cost is a touch greater, and also this procedure continues until the time comes for the loan to be paid off. That payment generally happens within one year of when you vacate the residential property or when you die. As soon as a reverse home loan is signed up versus the title of your residence, you might be unable to use your home to protect any type of future borrowing.

Some Of The Common Reverse Mortgage Misconceptions And False Impressions

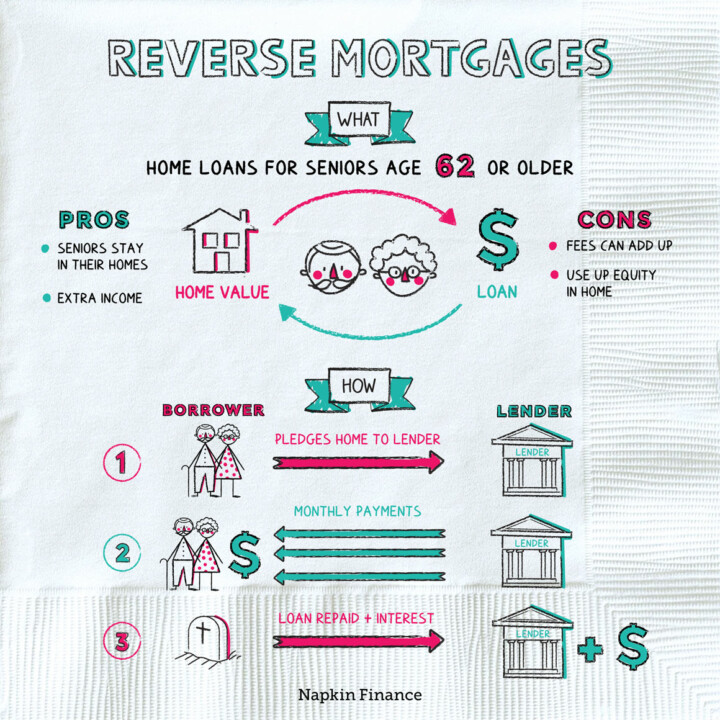

If you believe a reverse home loan may help you stay in your residence with retirement, ensure you understand the threats and rewards so you can make a better-informed decision. A reverse home loan can transform your home right into a consistent supply of money, however it can be pricey and also lugs some dangers. A Shared Gratitude Home loan thinks about the gratitude in worth of your house between the moment the loan is signed and also the end of the finance term. The lender obtains an agreed-to percentage of the appreciated value of the financing when the car loan is ended. Prior to you choose to get a reverse home loan, ensure you consider the advantages and disadvantages very carefully.

On your reverse home loan application, you need to include all the people detailed on your residence's title. All these people need to go to the very least 55 years of ages to be eligible. Nonetheless, this can be done using other funds or by re-financing through a traditional home loan. The finance is protected versus real estate you, or your partner, own in Australia. You pay a cost for the purchase and to get your residence valued (as an overview, around $2,000).

You can use the cash you get from a reverse home loan to do this. This implies that neither your neither your beneficiaries are personally accountable for any quantity of the mortgage that Hop over to this website surpasses the worth of your home when the loan is settled. Another common reverse mortgage myth is that if one person passes away, their partner is forced to move out. The making it through partner is under no commitment to move out or make any payments till they move or offer the residence. The MoneySmart website has a valuable reverse home mortgage calculator that demonstrates how much of your home you'll possess after different funding durations based on factors such as age, house worth, rate of interest and costs.

The Ideal Borrower

The reverse mortgage quantity available to you expands on the extra equilibrium but that is not "passion" being paid to you. Think of the line development rate much more like a boost in your credit line. If you were to take a line of credit with a preliminary draw of $70,000, the finance requires you to make no month-to-month payments yet you can make any kind of settlement in any type of amount you desire at any time. Nonetheless, it is necessary to note that any staying equity that is left after the lending is repaid will certainly be returned to the customer or his or her heirs. A routine home loan compounds on a reduced figure each month. When you get a reverse mortgage, you can take the cash as a round figure or as a credit line anytime you want.

About Government

Funds from a reverse mortgage can influence eligibility for need-based retired life earnings like Medicaid and also Supplemental Protection Income. There are a variety of reverse home mortgage rip-offs that victimize senior citizens who require cash to cover living expenditures. For many homeowners, nonetheless, the negative aspects of a reverse mortgage exceed the benefits. Think about these dangers prior to getting a reverse mortgage against your house. If the value of your house falls below the reverse mortgage equilibrium, your http://rowannyzg378.iamarrows.com/todays-mortgage-prices successors just need to pay the worth-- not the full outstanding equilibrium.